By Cliff Shrew – Jan 14, 2021, 5:00 PM CST

In Namibia, an African venue that is being set up as the scene of the world’s next—and possibly last—major onshore oil discovery, the oil and gas rights to an entire 8.5-million-acre sedimentary basin are owned by a single, small company.

Now, Wood Mackenzie, the most trusted name in oil and gas resource assessments, has issued a report stating that this same basin is analogous to three world-class basins, including the $540-billion Midland Basin in Texas.

The rig is now on-site, and the drilling has just begun on what could be the most exciting onshore oil play in decades. They’ve spudded their first 6-2 exploration well and are looking at three wells, back-to-back and 400km of 2D seismic over the next 2 quarters.

One of the most respected petroleum geochemists in the world, Dan Jarvie, came out of retirement for this play and believes this could be one of the largest oil basins worldwide, and his conservative estimate is that it could hold over 100 billion barrels of oil.

Just 40 days from now, the first well should be complete …

And just a few weeks after that, the analytical results should start coming in.

This could become a New Year bonanza for an oil and gas industry that has seen “discovery” become an obsolete word.

The bonanza gets multiple times bigger when we’re talking about a junior company with the kind of upside only a junior player can have …

A discovery barely moves the needle on an integrated supermajor that’s typically involved in drilling a basin of this scope and scale.

But for a junior, even the start of a drill can have maximum impact on share prices…

The basin that’s caught the attention of Wood Mackenzie is the Kavango Basin in Namibia and Botswana.

And the junior company stealing the show is Reconnaissance Energy Africa.

As the drilling starts, here are 5 reasons to put Recon Africa on your watchlist:

#1 This ‘African Permian’ Play Is Considered Analogous to the Midland Basin

Massively underexplored Africa is most likely the only place in the world left where we can possibly anticipate a major onshore oil and gas discovery. If that ends up being Namibia–all the more exciting. This under-explored country has never produced a single barrel of oil in its history. Either onshore or offshore and has excellent fiscal terms and infrastructure.

Exxon (NYSE:XOM) has already scooped up an additional 7 million net acres offshore …

But onshore, it’s all about Recon Africa, which strategically swooped in to acquire the rights to the entire Kavango sedimentary basin from Namibia all the way to Botswana.

That’s a basin over 8.5 million acres, almost the size of Switzerland.

And it’s analogous to three major world basins, according to Wood Mackenzie: The Midland Basin in Texas, the Southern North Sea Basin in the Netherlands and the UK, and the Doba Basin in Chad, Africa. And we are talking about CONVENTIONAL production here, no fracking, low water use, ‘normal’ decline curves, and low cost per BOE. For us in North America, it may be a memory, but all major basins begin their life with conventional production, unconventional / shale coming as the last gasp late in life. Production in the Midland Basin began in the ’30s, unconventional just a decade or so ago.

Source: Wood Mackenzie/Recon Africa

World-renowned geochemist Dan Jarvie puts Kavango’s potential oil generated at an estimated 100+billion barrels—

When Kavango first came to the world’s attention a few years ago, another world-renowned geologist and geophysicist, Bill Cathey, who works with the oil and gas supermajors, studied the basin and said: “Nowhere in the world is there a sedimentary basin this deep that does not produce commercial hydrocarbons.”

Then, Jarvie, a key force behind the Barnett Gas play and former chief geochemist for EOG Resources, jumped in on RECO as a shareholder because he saw a “very strong, independent junior explorer… sitting on a sedimentary basin that rivals South Texas in a massively underexplored region”.

The estimates here have gone from 12 billion barrels to 18 billion barrels to 100+ billion.

That makes for an exciting first drill.

Jarvie’s own estimates 100+billion barrels of oil equivalent are based only on 12% of Recon Africa’s total holdings.

#2 Analyst Coverage Is Decidedly Bullish—It Just Nearly Doubled

Haywood is all over this one.

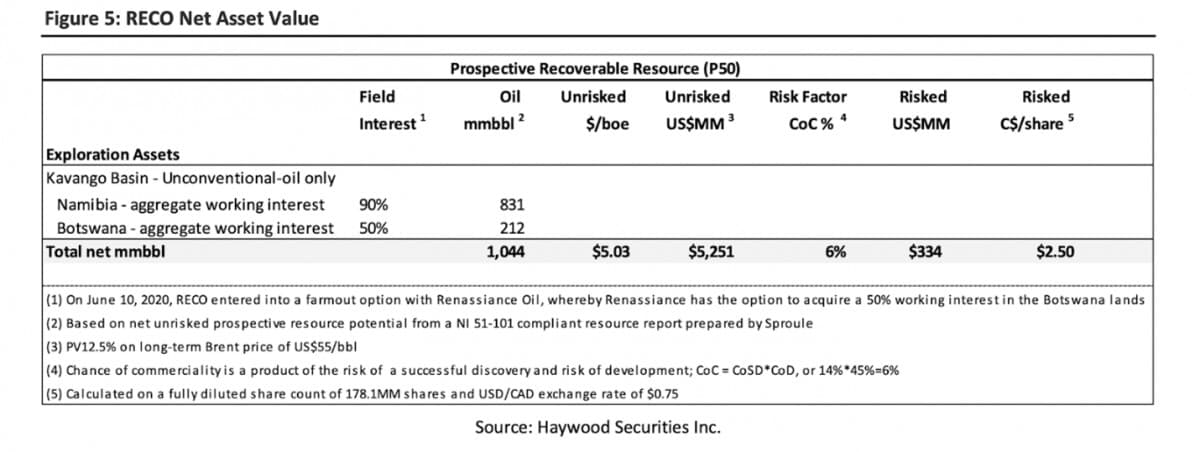

In early November, Haywood initiated coverage with a short-term $2.50 price on RECO because the company is “set and funded to de-risk a potentially material resource play onshore Namibia and Botswana with 1,348 mmbbls/58.1 Tcf, a conservative estimated prospective recoverable resource (gross).”

In arriving at its 12-month target price of $2.50/share, Haywood has risked this upside potential by a 6% chance of commercialization. In other words, they’re playing it uber-cautious with the $2.50 price tag. The potential upside for a junior company sitting on a supermajor basin all by itself is rather mind-blowing.

But in December Haywood raised its short term price target to $4.00 per share.

More to the point, Haywood recommended “accumulating a position ahead of drilling/evaluation news flow in H1/21 aimed at proving up the presence of a working hydrocarbons system, which if confirmed, should provide abundant opportunities for further exploration and appraisal drilling”.

“On a successful discovery, attractive fiscal terms should help to facilitate the development of the basin, thereby increasing the chance of commercialization and shareholder value”.

Haywood is also hanging on Dan Jarvie’s expertise here, with good reason. So, given the scale of the basin–again, we’re talking about 8.5 million acres–a discovery would present manifold opportunities for strategic joint ventures for further de-risking–without share equity dilution.

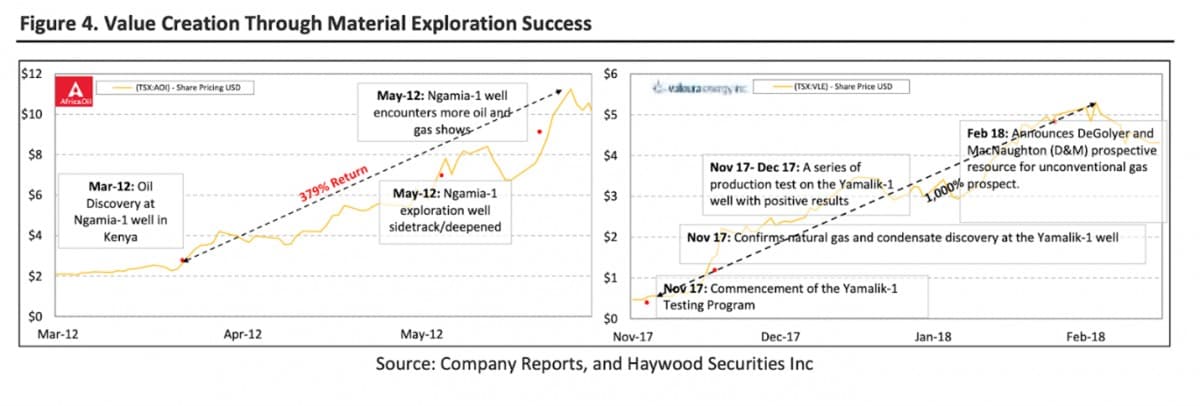

In its analysis, Haywood notes the 1,000% return potential for junior oil discovery projects during the exploration phase. And in the same breath, calls RECO an “attractive high-risk/high-reward investment opportunity” that could “experience “rapid value accretion” on success and/or anticipation of success.

It could be worth “multiples of its current valuation”, says Haywood.

And now, that story just got even better ….

In late December, when the drill rig arrived on site, Haywood nearly doubled its short-term price target from $2.50 to $4.00.

#3 Drilling Just Started ….

With the drill bit just hitting the ground on this massive African Permian play, If Dan Jarvie Is Right, RECO could end up going from a small-cap to a multi-billion-dollar company. And we’ll find out pretty quickly.

Jarvie charts it out like this:

And if the analysis is right about how much oil potential this play has, and development costs look anything close to this ….

Then early investors could be oil millionaires if this turns up a major discovery.

Torridon Investments has also initiated coverage, calling Recon Africa a “corporate story with a dedicated and internationally first-class management and technical team”.

“They’re implementing the same plan in Namibia … that similar companies successfully have done in the US. However, Namibia is cheaper to operate in, thus opex relative to a barrel can be lower than in the US. Also, more net revenue from a unit of gross stays in the company coffers given the favourable royalty regime,” Torridon notes.

For these exploration plays, it’s all about the speed of de-risking, and this one is fast-paced. Not only have the estimates just kept rising profoundly but RECO is on track to keep de-risking in a short period of time.

That’s why Haywood is eyeing the potential here for material near-term upside.

And the catalysts are all there, with the drill bit already hitting the ground in a 6-2 well spud.

Next comes 2D seismic acquisition and interpretation in Q1 2021, followed by 6-2 well evaluation and drilling of two other back-to-back wells in the same quarter.

By the second half of this year, it’s likely RECO will already be in JV discussions if drilling goes as planned.

#4 This is the grand oil lottery

This is the oil lottery, but Recon Africa is not your average wildcatter.

This is something entirely different.

This is one of those oil opportunities that almost never comes around.

This is a “high-conviction play”, according to Torrindo’s coverage, with a basin that is “one of the most significant underdeveloped basins of such depth globally”.

“The significance of this geological formation is that ALL such basins in the world with similar depth and general geological characteristics produce commercially viable hydrocarbons.”

This where some of the world’s most respected names in the industry come together to find the next—and possibly last—huge, onshore oil discovery, putting Namibia on the oil map for the first time in history, and possibly helping RECO evolve into a major oil company.

Recon Africa has put together a veritable “who’s who” exploration and technical team to move this project forward with some of the most qualified and successful oil “finders” in the business.

- Jay Park, RECO COB and director, is a veteran energy lawyer with tons of Africa experience and was designated Queen’s Counsel in Canada in 2011. He’s advised oil companies and governments in 50 countries, and he has a following of the best of the best.

- Scot Evans CEO, Geologist, new fields expert, is an energy industry leader with a combined 35 years of experience with Exxon, Landmark Graphics and Halliburton.

- Daniel Jarvie is globally recognized as a leading analytical and interpretive organic geochemist of Barnett Gas fame, and “Hart Energy’s Most Influential People for the Petroleum Industry in the Next Decade.”

- Nick Steinberger, a world-class drilling completion expert and manager of the drilling company; yes Recon Africa owns its own rig that if picked up for a song in the downturn

- Bill Cathey is a geophysicist to the supermajors, including Chevron, ExxonMobil, ConocoPhillips … major and large

This is the best of the best–all of them confident in the chance of discovering the largest oil play in the last 20 to 30 years.

But with the drill already hitting the ground, early-in opportunities are dwindling.

And still, their stock is way under the radar with no valuation for discovery. That’s exactly the setup that rarely comes along: A dream team, a massive basin all to a single junior, and estimates by first-class geoscientists that make this potentially more rewarding than any oil play this decade. For Haywood, among others, it’s a risk worth taking … right now, while it’s still in this price range.

**IMPORTANT! BY READING OUR CONTENT YOU EXPLICITLY AGREE TO THE FOLLOWING. PLEASE READ CAREFULLY**

Forward-Looking Statements. Statements contained in this document that are not historical facts are forward-looking statements that involve various risks and uncertainty affecting the business of Recon. All estimates and statements with respect to Recon’s operations, its plans and

DISCLAIMERS

ADVERTISEMENT. This communication is not a recommendation to buy or sell securities. Oilprice.com, Advanced Media Solutions Ltd, and their owners, managers, employees, and assigns (collectively “the Company”) have been paid by Recon seventy thousand U.S. dollars to write and disseminate this article. As the Company has been paid for this article, there is a major conflict with our ability to be unbiased, more specifically:

This communication is for entertainment purposes only. Never invest purely based on our communication. We have not been compensated but may in the future be compensated to conduct investor awareness advertising and marketing for TSXV:RECO. Therefore, this communication should be viewed as a commercial advertisement only. We have not investigated the background of the company. Frequently companies profiled in our alerts experience a large increase in volume and share price during the course of investor awareness marketing, which often end as soon as the investor awareness marketing ceases. The information in our communications and on our website has not been independently verified and is not guaranteed to be correct.

SHARE OWNERSHIP. The owner of Oilprice.com owns shares of this featured company and therefore has an additional incentive to see the featured company’s stock perform well. The owner of Oilprice.com will not notify the market when it decides to buy more or sell shares of this issuer in the market. The owner of Oilprice.com will be buying and selling shares of this issuer for its own profit. This is why we stress that you conduct extensive due diligence as well as seek the advice of your financial advisor or a registered broker-dealer before investing in any securities.